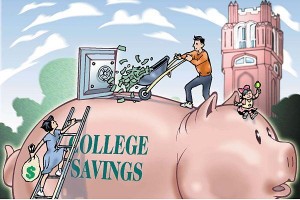

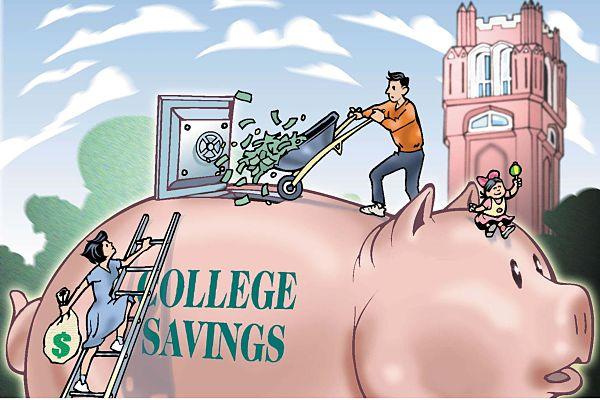

Saving for education is the most important form of saving as the future of the child depends upon it. It ensures that the education is not sacrificed because of lack of money.

Saving for education is the most important form of saving as the future of the child depends upon it. It ensures that the education is not sacrificed because of lack of money.

Higher education is getting expensive these days and people are finding it difficult to pay for it easily. One can manage to afford their higher education if they set aside some money and build savings for the same. If you start saving early, you can start with smaller amounts and eventually save a lot in the end. The savings you do will add up compound interest giving you a considerable amount of profit by the time you join a college. You do not even need to ask someone for money once you have your own savings.

One must look for regular saving goals so that the amount of savings is added up to fund the education. You must plan for your future so that you do not have to leave a college just because it is difficult for you to afford it. In order to save enough amount of money, you can also take the help from the automatic electronic transfers where a particular amount is deducted from your paycheck every month and is deposited in an account where your savings for the education is there. This helps you save a considerable amount of money when you are planning to save for your education or for some other financial goal.

When you make an online account of the bank to do the savings, you must add a nickname to the account and mention the name of your children or grandchildren. The online banking is carried on smoothly this way and is helpful if you are trying to save. These online accounts also send you reminders if you miss your payments and you know what are you saving for and for whom are you doing so.

If you are a parent, and are saving for your child’s education, then you must ask your child to save for his education from his allowance too. This can be started at an early age as it teaches the children to save and manage finances. The sense of responsibility is there in children and it is easier for them to realize the financial condition at an early age. The children also tend to be a little proud of them because they have contributed to their education from their own savings.

For the ones who want to save some money for the education has many options so that they can save easily. Several plans and accounts that are offered to the people and they use them to deposit their money in that. There are certain eligibility criteria and limits on the contributions made in these accounts and so, one should contact a professional and clear all the doubts before taking one. You can know about the terms and conditions along with the fees involve and assess whether it is meant for you or not. Irrespective of which type of plan you go for, funding for education is a very important thing and one must start doing that early so that the education is not compromised because of lack of funds.

When the students move out if home and start living away from home, they tend to make their own financial decisions and learn how to manage their finances. They start learning how to do so over time and become quite smart about their approach. There are certain ways that help them manage their finances when they are away from home:

Checking Account: One can open a checking account in case the electronic transfers or purchases are to be made. The deposit and the withdrawal of money become easy when one has a checking account. The ones who have a debit card can shop around with it just as if they do while shopping with cash. The fees and the charges associated with the card should be read properly and then it should be signed up.

Ways to Save: The students can also open a saving account that will help them save and earn interest on the money at the same time. They can help the student to save the tuition fee or the money required for the textbooks. Emergency monetary requirements can also be met with the help of these savings.

Student Credit Card: There are student credit cards that are offered to the students so that they can build their credit histories and can manage their finances at an early age. They learn how to handle the responsibility of a credit card and avoid overspending.

Very often people come across situations during which they need to access quick funds. The main concern is the short term for the loan. Since the difficulty in repaying the loan in a short time is felt, many people look for fast loans with the provision of repayments in installments. These fast loans cannot be accessed by poor credit borrowers. With a good credit score, these loans are easy to obtain. The banks and other financial institutions can be approached for fast loans with monthly repayments.

Very often people come across situations during which they need to access quick funds. The main concern is the short term for the loan. Since the difficulty in repaying the loan in a short time is felt, many people look for fast loans with the provision of repayments in installments. These fast loans cannot be accessed by poor credit borrowers. With a good credit score, these loans are easy to obtain. The banks and other financial institutions can be approached for fast loans with monthly repayments.

Fast loans are secured loans

Most of these offers are personal loans and however, there are loans which are granted for specific purposes like the purchase of autos and so on. Theoretically, any loan can be considered as fast loan allowing monthly payments. But, the fast loan with monthly payments has some basic features. The offer is a secured loan. You can submit your home equity, financial instruments, and valuable jewelry and so on as security for the loan. If the loan is intended for specific purchases such as a vehicle, then the vehicle can be submitted as collateral for the loan.

Committing to monthly installments is a serious issue. The offer is ideal for those with secured employment and regular income. The interest rates are determined based on the credit report of the borrowers. With good credit ratings, you can get eligible for loan with lower interest rates. The fast loan with monthly payments can be beneficial to you only if the interest rates are nominal as the stress due to regular monthly payments is minimized. The term of the loan is around 2 to 5 years and lower in certain cases. The amount you commit to pay every month determines the loan term. The interest rate is lower if the loan term is longer.

Though there are some similar basic features for all fast loans with monthly payments, each of the offers differ in certain factors. To get one of the best offers, you have to approach the loan originator. You can expect to get quick access to a good offer with flexible terms and reasonable interest rates, if your credit score is excellent. The fees for originating the loan, the charges for the process and other fees such as commissions and so on will be affordable if the loan originator is approached for the loan. As you submit the application for the fast loan with monthly payments, the lender reviews your application here.

The lenders check your credit record and other details that are required for the loan approval. The interest rates and repayment details will be intimated to you as soon as your loan application is approved. Evaluation of the collateral that is submitted for securing the loan is done as a part of the loan underwriting process. Your debt to income ratio is scrutinized to ensure that you can afford the loan. With a cleaner credit record, you can enjoy the benefit of lesser fees. Banks and other government financial organizations can be approached for the offer as you can get the loans for lower interest rates than you can get from private lenders.

FHA 203k loan can be borrowed to purchase a home or to improve the home if needed. A clear understanding of the offer is necessary to understand whether you will be benefited by the offer or not. The eligibility criteria and the extra costs for the offer should be understood before you opt for the loan. The interest rates for FHA 203k loan are higher than charged for other types of FHA loans. This makes the borrower pay more for the loan than its real worth. The lenders do not have much risk as there is guarantee for the loan.

FHA 203k loan can be borrowed to purchase a home or to improve the home if needed. A clear understanding of the offer is necessary to understand whether you will be benefited by the offer or not. The eligibility criteria and the extra costs for the offer should be understood before you opt for the loan. The interest rates for FHA 203k loan are higher than charged for other types of FHA loans. This makes the borrower pay more for the loan than its real worth. The lenders do not have much risk as there is guarantee for the loan.

The costs involved in the offer

This all in one mortgage loan is backed by the U.S. Department of Housing and Urban Development and the loan is offered by the mortgage personal loans bad credit lenders. Since the loan is insured by the federal government, the approval does not get delayed. There are closing costs for the loan which you can pay eventually. With the origination charges and the insurance for the loan, the lender is protected though the borrower does not repay the loan as specified in the loan agreement. The charges due to the improvement work should be considered.

The plans of improvement are reviewed by one of the approved consultants of FHA and the approval is granted as per the review. The repair work is also supervised in every stage which increases the cost of the loan. The borrower is required to bear the cost due to the appraisal as well. All these should be considered while you estimate the cost of the loan and your ability to make repayments due. Safety and health issues are to be addressed and they should adhere to the building codes specified.

Electrical problems and lead points are some of the important items that are included in the project list. There are restrictions to the offer and you cannot get approved for the loan if you wish to make some profit out of your investment in the property. You need to be a owner occupying the house to be eligible for FHA 203k loans. The offer cannot be obtained for the purpose of investments. If you decide to make additional structure to your house that you have rented out, you can get the offer of FHA 203k loan.

There is the minimum amount specified for the personal loans no credit check and the borrower is supposed to complete the mentioned renovation or repair work within the set time. The loan is initiated to support in the purchase of a home or to do the renovations that are essential. You cannot think of using the loan amount for luxury items. However, you should also remember that you cannot get the needed loan amount if you underestimate the cost of the renovation work. Besides your financial counselor, it is important to consult a good contractor to get the required financial support from FHA 203k loans.

It’s extremely unfortunate, but with rising living costs, many people who’ve retired are discovering they have to take on work to make ends meet. Sometimes pensions may just about cover expenses, but not provide people with the cash to enjoy things they’ve always wanted to do. In other scenarios, retirees’ income isn’t even enough to pay for food, heating and the plethora of other expenses associated with modern day life. Often, discovering they have to go back to work can be very upsetting for people. But there is a great range of options available if individuals need to make some extra cash.

It’s extremely unfortunate, but with rising living costs, many people who’ve retired are discovering they have to take on work to make ends meet. Sometimes pensions may just about cover expenses, but not provide people with the cash to enjoy things they’ve always wanted to do. In other scenarios, retirees’ income isn’t even enough to pay for food, heating and the plethora of other expenses associated with modern day life. Often, discovering they have to go back to work can be very upsetting for people. But there is a great range of options available if individuals need to make some extra cash.

One great way to earn some extra money is to utilise the skills people already hold. For example, nurses can find an abundance of work by picking up a few temporary shifts here and there. Home care services also require nurses, and a variety of shift lengths allow people to choose the best working pattern to suit their needs. Likewise, retired accountants can find work bookkeeping or helping contractors fill out their self-assessment forms. Other retirees who have plumbing or carpentry skills make the ideal local handyman for neighbours to call on, whilst those who have creative expertise, such as photography, could turn to wedding and event photography to make some extra money.

Another great option for innovative and entrepreneurial retirees’ is to set up a small home business. Those with good English and writing skills could become copywriters, creating content that can be used for websites and press releases around the world. Individuals who love crafting could set up an eBay or Etsy shop and sell their work, whilst keen bakers and cooks can turn ingredients into artisan products to be sold at farmers’ markets or to local restaurants.

For those not wanting to set up a business, part-time work might also be found close to home. Many supermarkets and high street stores have policies encouraging the hiring of older people, so it’s worth visiting these shops and taking a moment to speak to a manager to see if any vacancies are available. Local newspaper and newsagent windows are also a great source of wanted ads, and part time or temporary work can often be found listed there.

It’s important for anyone wanting to take on extra work to pay very close attention to their finances and ensure they don’t start to earn too much. Whilst many people want to earn a little money to supplement their income, earning too much could put pensions into jeopardy, so it’s crucial to do a little research and discover the personal income limits before undertaking work. Unfortunately, there are also a few unscrupulous individuals out there waiting to take advantage of older people, so individuals wanting work should never send money to agencies claiming to find jobs for a fee.

Taking on a small job when retiring can actually be very enjoyable, not only providing a little bit of extra cash, but also giving people an entirely new social circle; and, with retiring being an ideal time to make a career change and try something new, getting a job can bring about a new lease of life.

“Having a lodger” or “taking lodgings” are phrases that bring to mind the Victorian era, when widowed ladies rented out rooms in their city homes to single men and women. Though private homes and apartments have since become the norm, the idea of renting a single room in a private home has been steadily increasing, due in part to the difficult economy. For homeowners, the idea of renting out a room has become more and more appealing, so much so that the number of private homeowners renting out a spare room in their home has more than tripled in the past year.

“Having a lodger” or “taking lodgings” are phrases that bring to mind the Victorian era, when widowed ladies rented out rooms in their city homes to single men and women. Though private homes and apartments have since become the norm, the idea of renting a single room in a private home has been steadily increasing, due in part to the difficult economy. For homeowners, the idea of renting out a room has become more and more appealing, so much so that the number of private homeowners renting out a spare room in their home has more than tripled in the past year.

Financial advantages of renting out a spare room

The extra income generated on a monthly basis is one of, if not the, main reasons that people choose to open their homes to a stranger. The amount of rent being charged for a room will vary depending not only on the size of the room and its amenities, but also on where the home is located. A bedroom with bathroom and kitchen privileges may run around $200 per month while a room with a private bathroom en-suite or possibly an efficiency layout with a small refrigerator and microwave could run as much as $500 per month. The type and amount of furnishings, as well as the utilities included will also affect pricing.

Renting out a spare room also allows the homeowner to receive a break on their income taxes by deducting part of their home ownership expenses. Real estate taxes and home mortgage interest are two areas where dividing the property into effectively two homes can save when it comes to tax time. Deductions may also be taken for general maintenance, expenses and repairs to the home, including utility bills and repairs to appliances, as long as these are available to the entire home. Installing utility services directly to the room being let may also be deducted, for example the installation of a cable or phone line.

Financial costs of renting out a spare room

Choosing to rent out a room in the home means the homeowner may have to invest before the profits roll in. The room needs to be properly and simply decorated with a sleeping area the primary focus and a seating area a close second. This may mean carefully selecting furnishings and investing in pieces such as a sleeper sofa or a built-in Murphy bed that are both functional and attractive. Room design and décor may need to be quite different in a rented room than it would be in the rest of the home, with furniture choices and layouts more like those in a studio or efficiency apartment than in a traditional bedroom. The homeowner can save on the furniture by watching for sales and taking advantage of free delivery if available. Neutral color palettes and wood furniture pieces are universally appreciated and allow the tenant some leeway to express themselves and their style by adding accessories and personal items.

Other financial considerations include legal expenses, such as credit checks on prospective tenants and extra home insurance reflecting the new rental status of the property.

Saving for education is the most important form of saving as the future of the child depends upon it. It ensures that the education is not sacrificed because of lack of money.

Saving for education is the most important form of saving as the future of the child depends upon it. It ensures that the education is not sacrificed because of lack of money.